Americans have accumulated additional savings during the pandemic, but that money is dwindling rapidly due to inflation.

About 70% of Americans use their savings to cover price hikes, a Forbes Advisor’s latest survey Infer 2000 American adults. Among those surveyed, older adults were more likely to say they left their savings intact.

In fact, the personal savings rate for April 2022 was 4.4% – the lowest level since September 2008 – down from 6% at the start of the year, according to Economic Analysis BureauA division of the US Department of Commerce.

Another concern: More participants told the New York Fed “Consumer Expectations Survey“Their financial conditions are worse now than they were a year ago. In fact, the average chance of missing a minimum debt repayment in the next three months rose 0.4 percentage point to 11.1%, according to survey results released on Monday.

“The median forecast for household nominal spending growth rose sharply to 9% from 8% in April,” the New York Fed said. “This is the fifth consecutive increase and the new rise for the series. The increase was most pronounced for respondents aged 40 to 60 years and respondents without a college education.”

The decline in savings and the rise in spending come at a time when the drums of stagnation are sounding. Case in point: nearly 70% of 49 respondents expect the National Bureau of Economic Research to declare a recession next year, According to a Financial Times poll published on Sunday; The survey was conducted with the Global Markets Initiative at the University of Chicago Booth School of Business.

Although some Americans have built up savings during the pandemic, with the help of COVID-related government benefits, those savings appear to be running out as people deal with higher prices.

Laura Feldkamp, a professor of finance and economics at Columbia University, suggested people try to renegotiate salaries with their employers. “The prices will not go down,” she said. “They never did.” She added that plunging into savings to counteract rising prices is not a sustainable long-term solution.

The increase in the cost of living is making Americans nervous. Inflation rose 8.6% year on year through May, the highest level since 1981. A US Consumer Confidence Survey It fell in May to a three-month low of 106.4. this One of many surveys Pointing to a pessimistic view by people of both their own finances and the US economy.

In the week ending May 29, grocery inflation hit a record 14.6% from a year ago, according to the latest survey by data company Numerator. The survey shows that middle income consumers Those who earn between $40,000 and $80,000 a year pay the largest price increases of all income levels.

““Cutting your budget doesn’t have to be a pain.”“

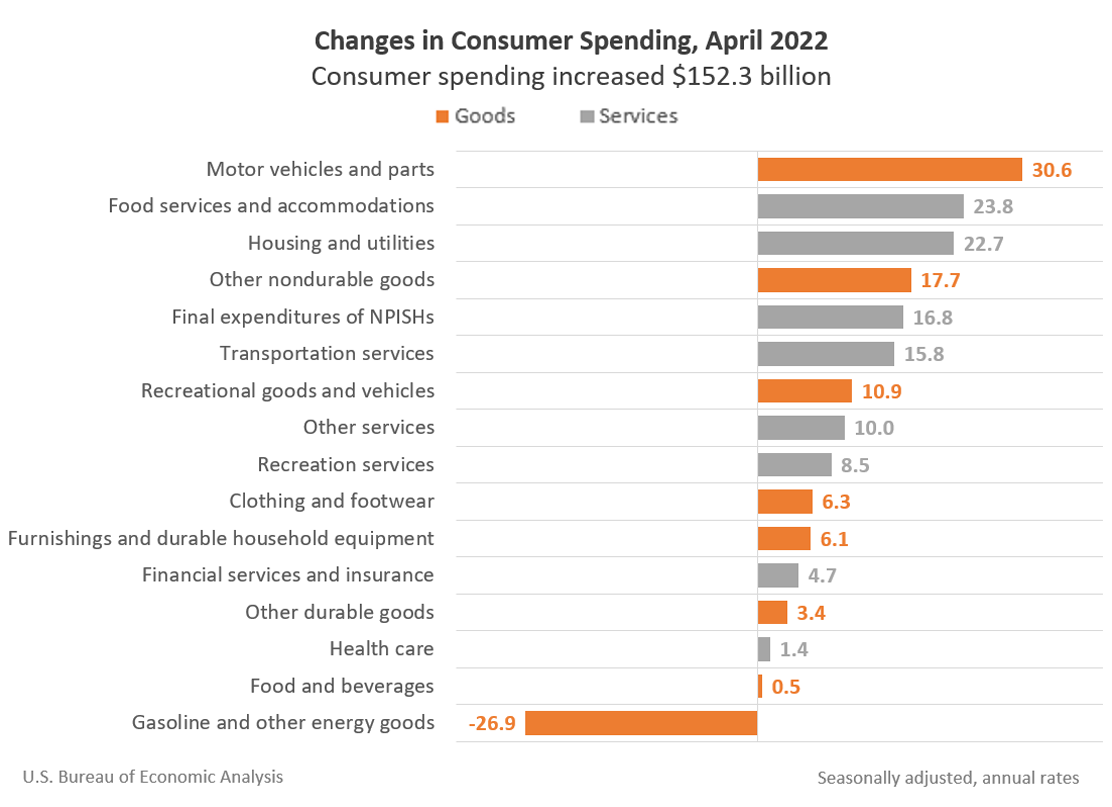

In April, consumer spending by 152.3 billion dollarsSeparate data from the Bureau of Economic Analysis found that people spend the most money on cars and auto parts, as well as food and housing. Compared to the previous month, consumption of gas and other energy decreased by $26.9 billion.

{kind=link}

On Sunday, AAA put the national average at $5.01 for a gallon of gasoline. That’s 20 cents higher than it was a week ago, 60 cents higher than last month, and about $2 more than the average of $3.07 a year ago, according to AAA data.

Thomas Scanlon, a financial advisor at Raymond James Financial in Manchester, Connecticut, said the time is right to adopt economic habits, such as borrowing from the public library rather than buying a book, and looking forward to free leisure activities such as visits to some museums and beaches.

Cutting your budget doesn’t have to be a pain, Scanlon said, “it can be an opportunity to spend quality time with friends and families.”

“Beer aficionado. Gamer. Alcohol fanatic. Evil food trailblazer. Avid bacon maven.”