Massive cuts on tech giants like Meta and Microsoft dominate headlines, but don’t tell the whole story. Here’s a complete picture of job cuts around the world.

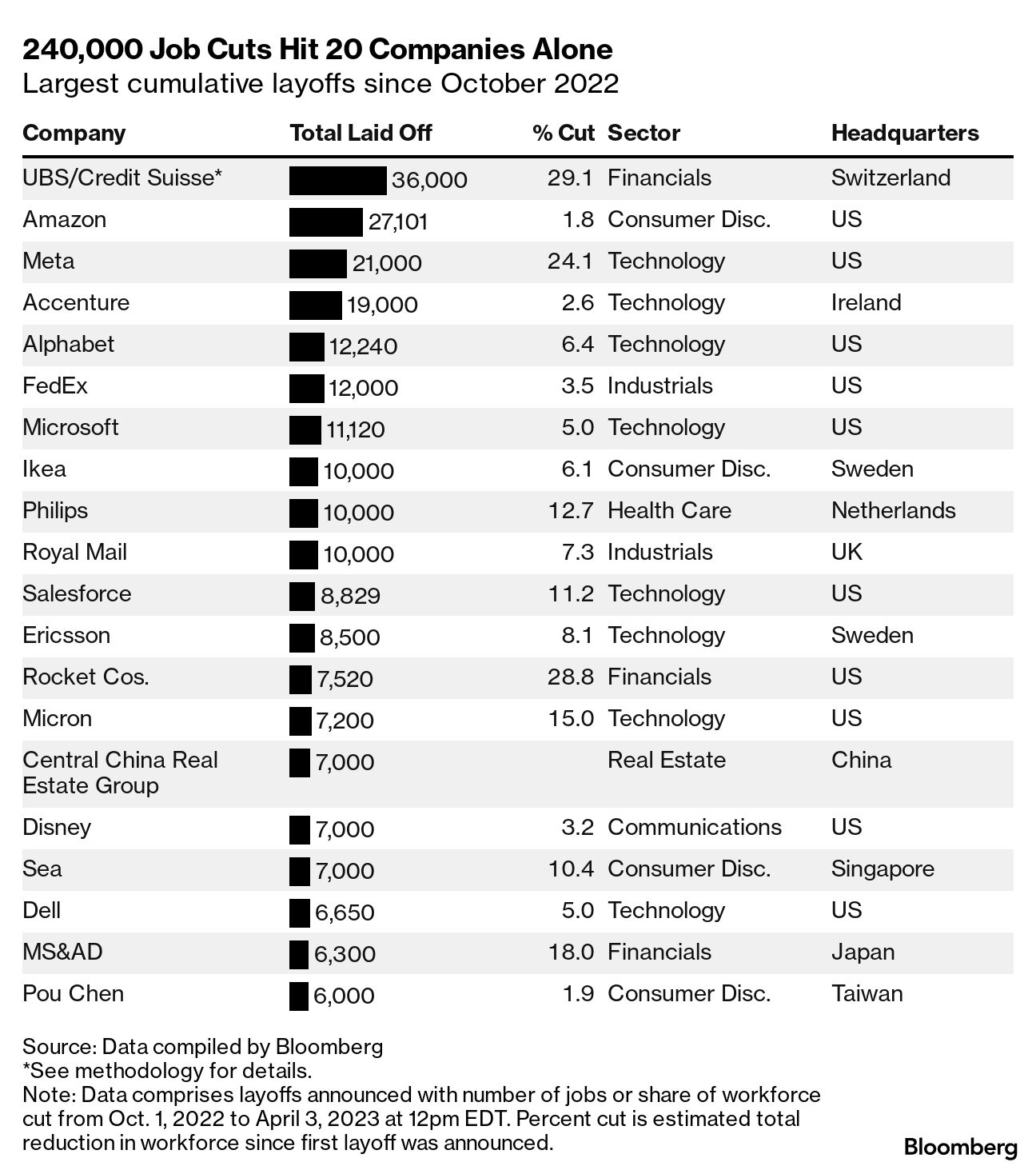

UBS Group AG’s reported plan to lay off up to 36,000 workers would make it the company that saw the largest job cuts globally in the past six months.

The cuts, which can reduce the combined workforce by up to 30%, are part of UBS’ takeover of longtime rival Credit Suisse Group AG. Credit Suisse chairman Axel Lehmann has apologized at the bank’s annual meeting of shareholders for failing to save the 167-year-old bank.

The layoffs come on the heels of last month’s Silicon Valley bank meltdown, which sent shock waves through an economy already shaken by mass layoffs and under pressure from central banks locked in a high-stakes battle with inflation — raising the risk of a recession even larger. job loss.

While the US economy has remained strong so far, adding 311,000 jobs in February after adding more than half a million jobs in January, central banks’ increasingly aggressive campaign to raise interest rates may expose more vulnerabilities in interest rate risk banks, such as SVB, and startups that rely heavily on venture capital funding to maintain operations and payroll.

The rush of layoffs that began late last year has not stopped, marking the worst start to a year since 2009, with 52,000 jobs lost in one week in January alone. Since Oct. 1, executives across industries have laid off nearly 538,000 employees worldwide, according to a comprehensive review of layoffs by Bloomberg News.

Weekly job cuts, their roots and flow across sectors

Note: Data includes layoffs announced with the number of jobs or share of the workforce reduced from October 1, 2022 to April 3, 2023 at 12 noon EST. Combined layoff data for the week ending on Sunday. Source: Data compiled by Bloomberg

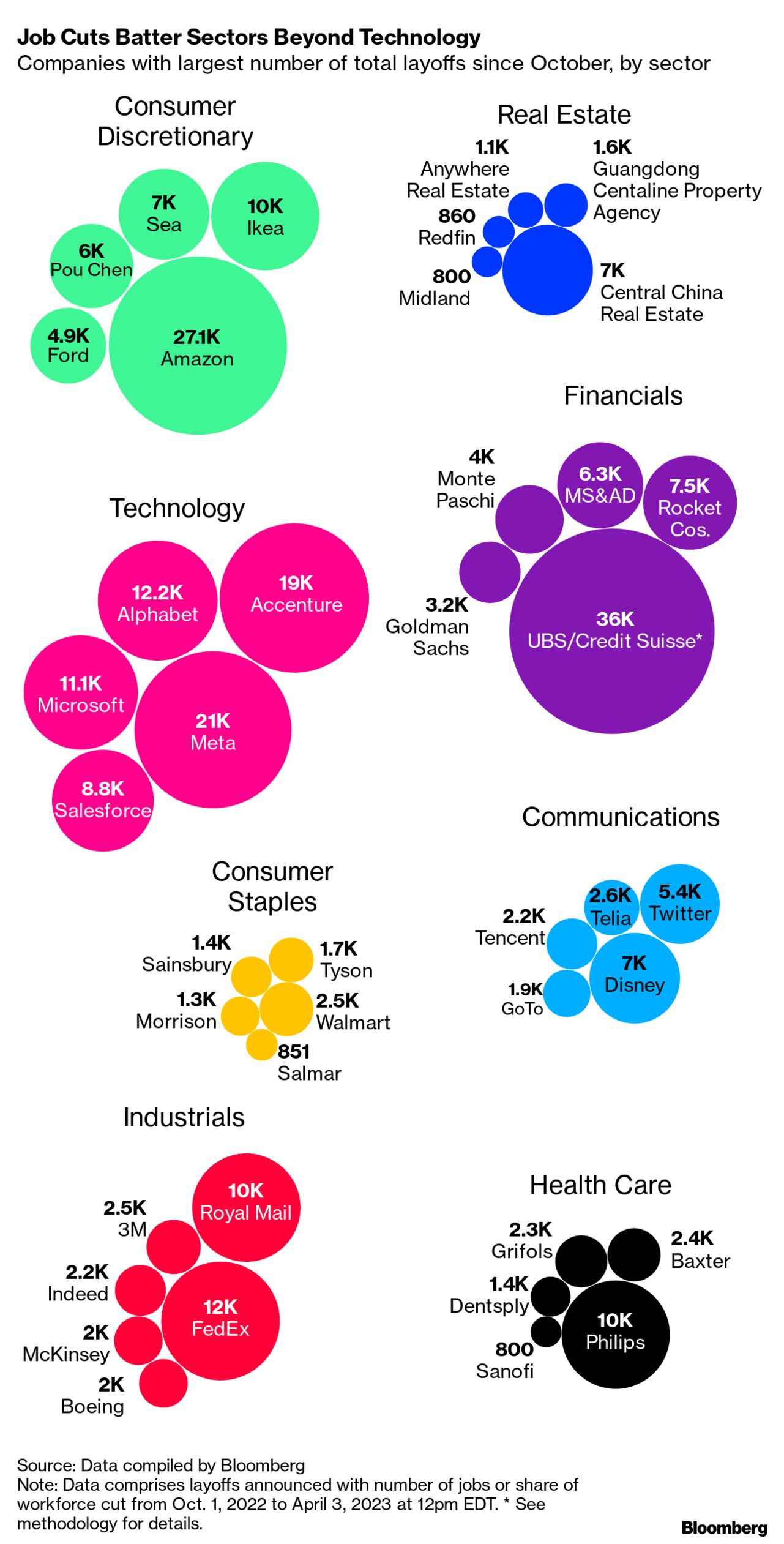

Second only to UBS, Amazon.com Inc. will cut nearly 30,000 jobs with its latest round of layoffs announced on March 20. Meta Platforms Inc. Third place, with 21,000 job cuts overall. But they’re just three of the 760 companies that have cut more than half a million jobs since October, with the average layoff leaving the company’s workforce 10% smaller, according to a Bloomberg analysis. Another 108 companies made cuts without specifying how many employees received pink slips.

The technology sector saw some of the biggest losses, accounting for nearly a third of all cuts. Company leaders said they increased capacity as demand for their services increased during the pandemic. The mass layoffs have stunned many Silicon Valley workers, who have long enjoyed generous wages and soft benefits. Management has promised investors a new era of austerity, with Meta CEO Mark Zuckerberg calling 2023 “the year of efficiency.”

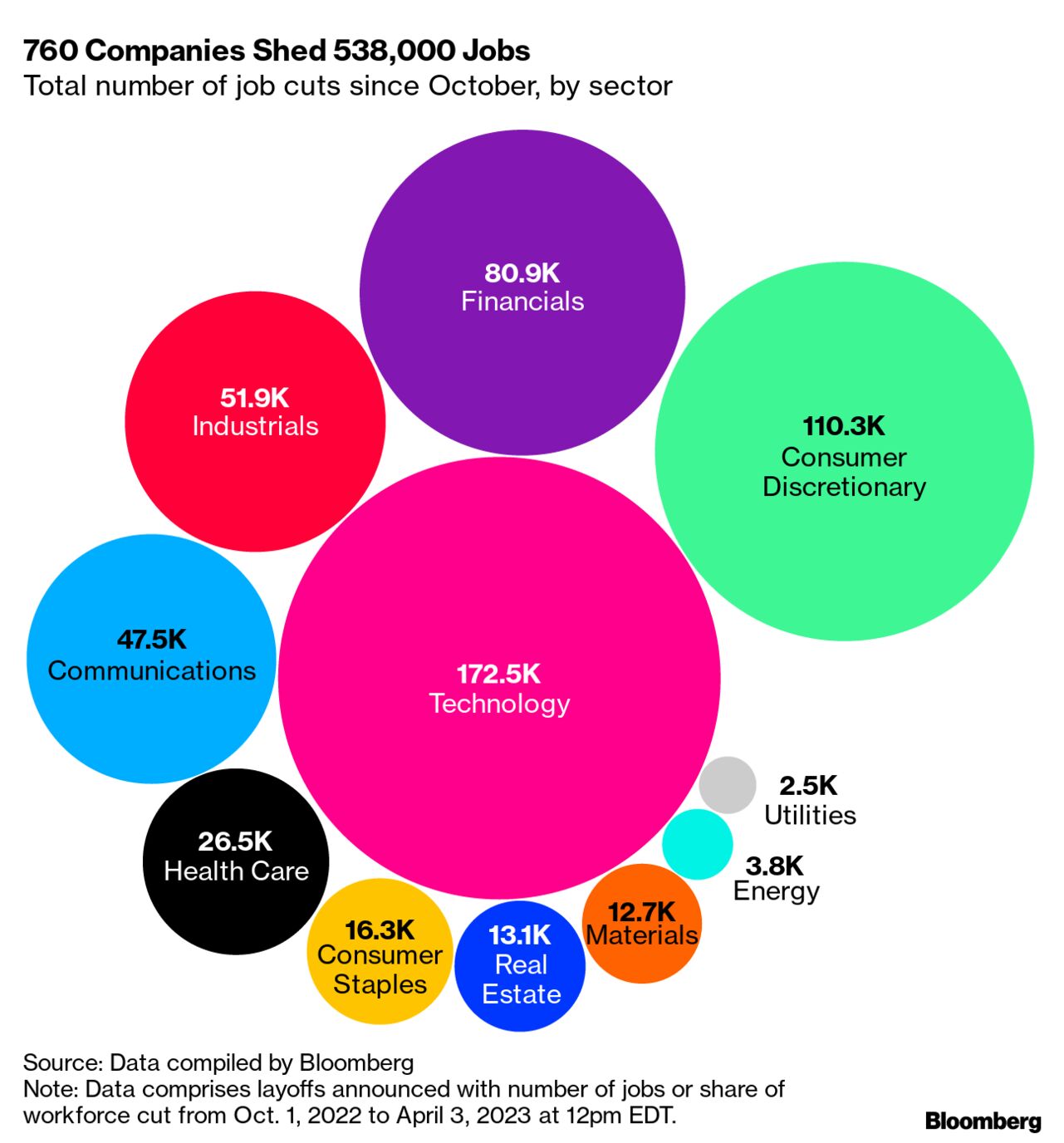

760 companies laid off 538,000 jobs

Total number of job cuts since October, by sector

Note: Data includes layoffs announced with the number of jobs or share of the workforce reduced from October 1, 2022 to April 3, 2023 at 12 noon EST. Source: Data compiled by Bloomberg

The carnage extends far beyond technology. Of all the cuts in which the share of jobs reported to have been eliminated or could be derived, the average tech layoff sent 10% of the company’s employees. In the telecoms, financials, healthcare, real estate, and energy sectors, average layoffs were as great or greater, although total job losses were lower. In health care, for example, the average drop in workers was 21% across more than 130 layoffs, driven by massive cutbacks at small startups like Rubius Therapeutics Inc. , which shed more than 80% of its staff in November.

The consumer discretionary segment has canceled more than 110,000 roles, as demand falters and sales at outlets such as Amazon fall short of expectations. Goldman Sachs and other big banks cut thousands of jobs despite a glimmer of hope on Wall Street from the soft landing.

Work cuts batter sectors far beyond technology

Companies that have seen the most total layoffs since October, by sector

Note: Data includes layoffs announced with the number of jobs or share of the workforce reduced from October 1, 2022 to April 3, 2023 at 12 noon EST. * See methodology for details. Source: Data compiled by Bloomberg

Energy companies were among the least affected, with fewer than 4,000 jobs cut. Oil majors such as ExxonMobil and Chevron posted record profits and announced massive share buybacks as Russia’s war in Ukraine sent energy prices soaring.

Across sectors, security and job stability have emerged as priorities for many workers. About 4 million American workers left their jobs in February, down from Covid-era highs although they still hover above pre-pandemic standards.

In general, layoffs have been significantly reduced. Nearly half of the job cuts were made by just two dozen companies, including big names like FedEx, Ikea and Philips.

240,000 jobs targeted 20 companies alone

The largest cumulative layoffs since October 2022

* See methodology for details. Note: Data includes layoffs announced with the number of jobs or share of the workforce reduced from October 1, 2022 to April 3, 2023 at 12 noon EST. Percentage cut estimates the total decrease in the workforce since the first layoff was announced.

Source: Data compiled by Bloomberg

More on Bloomberg

“Beer aficionado. Gamer. Alcohol fanatic. Evil food trailblazer. Avid bacon maven.”